The next recession will probably be caused by one of the following (from least likely to most likely):

3) An exogenous event such as a pandemic, significant military conflict, disruption of energy supplies for any reason, a major natural disaster (meteor strike, super volcano, etc), and a number of other low probability reasons. All of these events are possible, but they are unpredictable, and the probabilities are low that they will happen in the next few years or even decades.

emphasis added

Unfortunately, in 2020, one of those low probability events happened (pandemic), and that led to a recession in 2020.

2) Significant policy error. Two examples: not reaching a fiscal agreement and going off the “fiscal cliff” probably would have led to a recession, and Congress refusing to “pay the bills” would have been a policy error that would have taken the economy into recession.

That was written in 2013, and it appears once again that we’ve avoided the “default” policy error.

1) Most of the post-WWII recessions were caused by the Fed tightening monetary policy to slow inflation. I think this is the most likely cause of the next recession. Usually, when inflation starts to become a concern, the Fed tries to engineer a “soft landing”, and frequently the result is a recession.

And this most common cause of a recession is the current concern.

In the FOMC Minutes released last Wednesday, the staff predicted a “mild recession” later this year:

The economic forecast prepared by the staff for the May FOMC meeting continued to assume that the effects of the expected further tightening in bank credit conditions, amid already tight financial conditions, would lead to a mild recession starting later this year, followed by a moderately paced recovery. Real GDP was projected to decelerate over the next two quarters before declining modestly in both the fourth quarter of this year and the first quarter of next year.

emphasis added

And the FOMC members have been essentially projecting a recession for some time (although they avoid using the word “recession”). Here are their March projections for GDP and unemployment.

| GDP projections of Federal Reserve Governors and Reserve Bank presidents, Change in Real GDP1 | ||||

|---|---|---|---|---|

| Projection Date | 2023 | 2024 | 2025 | |

| Mar 2023 | 0.0 to 0.8 | 1.0 to 1.5 | 1.7 to 2.1 | |

1 Projections of change in real GDP are from the fourth quarter of the previous year to the fourth quarter of the year indicated.

| Unemployment projections of Federal Reserve Governors and Reserve Bank presidents, Unemployment Rate2 | ||||

|---|---|---|---|---|

| Projection Date | 2023 | 2024 | 2025 | |

| Mar 2023 | 4.0 to 4.7 | 4.3 to 4.9 | 4.3 to 4.8 | |

2 Projections for the unemployment rate are for the average civilian unemployment rate in the fourth quarter of the year indicated.

Since the unemployment rate was at 3.4% in April and depending on the growth of the civilian labor force in 2023, the FOMC is projecting between 800 thousand and 2 million jobs lost over the last two quarters of 2023. That is a clear employment recession.

One of the leading indicators for recessions is the yield curve. Here is a graph of 10-Year Treasury Constant Maturity Minus 2-Year Treasury Constant Maturity from FRED.

One of the leading indicators for recessions is the yield curve. Here is a graph of 10-Year Treasury Constant Maturity Minus 2-Year Treasury Constant Maturity from FRED.

My yield-curve indicator has gone Code Red. It is 8 for 8 in forecasting recessions since 1968 —with no false alarms. I have reasons to believe, however, that it is flashing a false signal.

…

The yield curve has now inverted for a ninth time since 1968. Does it spell doom? I am not so sure.

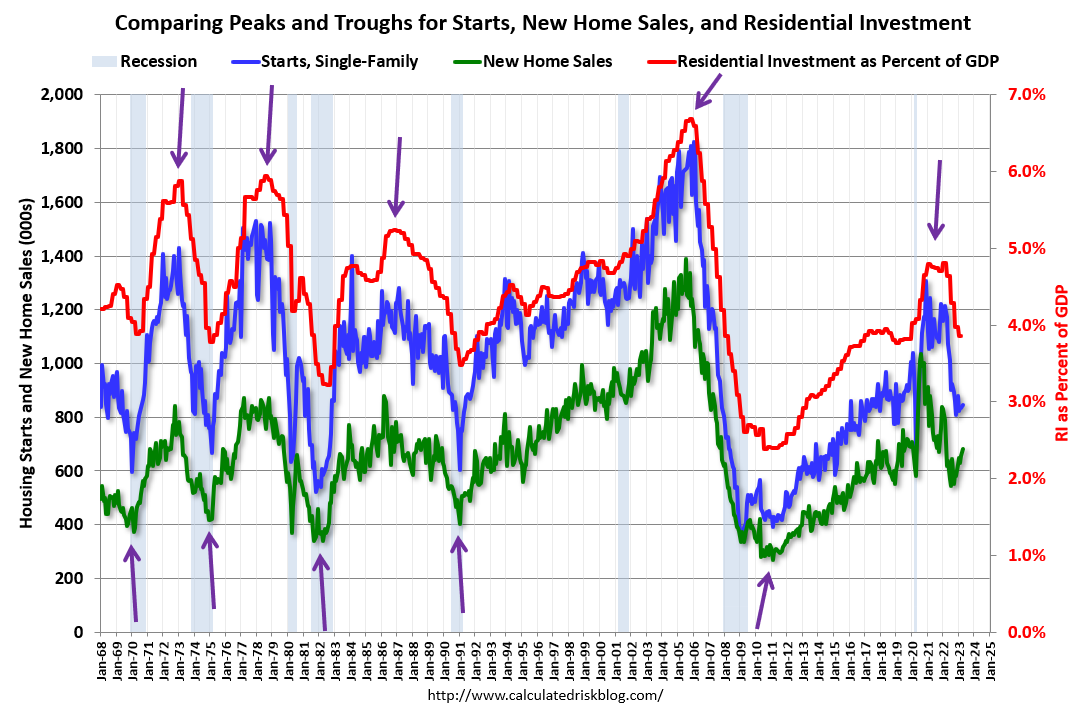

The arrows point to some of the earlier peaks and troughs for these three measures – and the most recent peak.

The arrows point to some of the earlier peaks and troughs for these three measures – and the most recent peak.

New home sales peaked in 2020 as pandemic buying soared. Then new home sales and single-family starts turned down in 2021, but that was partly due to the huge surge in sales during the pandemic. In 2022, both new home sales and single-family starts turned down in response to higher mortgage rates. Residential investment has also peaked.

This third graph shows the YoY change in New Home Sales from the Census Bureau. Currently new home sales (based on 3-month average) are up 4% year-over-year!

This third graph shows the YoY change in New Home Sales from the Census Bureau. Currently new home sales (based on 3-month average) are up 4% year-over-year!

A short term leading indicator I’ll be watching is the 4-week average of unemployment claims.

A short term leading indicator I’ll be watching is the 4-week average of unemployment claims.